U.S. Night Vision Equipment Market Revenue Insights

Market Statistics

Study Period

2019 – 2032

2024 Market Size

USD 2.8 Billion

2025 Market Size

USD 3.1 Billion

2032 Forecast

USD 6.4 Billion

Growth Rate (CAGR)

10.9%

Largest Region

South

Fastest Growing Region

South

Nature of the Market

Fragmented

Growth Forecast

Key Players

Key Report Highlights

Market Size and Forecast

Industry Trend

Regulatory Landscape

Demand Trend Analysis

Companies Recent Strategical Developments

Key Stakeholders

Voice of Industry Experts/KOLs

Future Opportunity

Explore the market potential with our data-driven report

U.S. Night Vision Equipment Market Future Outlook

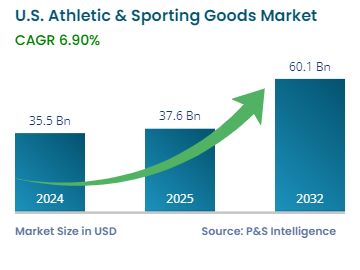

The U.S. night vision equipment market revenue in 2024 was USD 2.8 billion, and it will reach USD 6.4 billion by 2032 at a CAGR of 10.9% during 2025–2032. This is due to the rapidly increasing demand for security, rising engagement in outdoor activities by civilians, surging need for law enforcement, and advancing military technology. Night vision technology is expanding into sectors, such as hunting and navigation, apart from its long-established usage in surveillance and search & rescue operations.

The U.S. military and homeland security agencies widely use these products due to the increasing tension and security concerns at borders. Law enforcement agencies also depend on this equipment for crime prevention, border security, and tactical operations. The demand for thermal imaging cameras, scopes, and night vision goggles is also increasing in commercial applications, especially among outdoor enthusiasts and private security firms.

U.S. Night Vision Equipment Market Segmentation and Category Analysis

Product Type Analysis

Goggles are the leading product type, with a share of 45% in 2024 because these items serve military forces, law enforcement agencies, and tactical units. U.S. military forces extensively use NVGs because they allow hands-free operation for night activities, including navigation and surveillance. NVGs enable portability and unobstructed nighttime visibility, which makes them a key purchase area for law enforcement and military agencies in the country. This tactical equipment serves multiple defense functions, such as navy aviation operations and special force assignments.

Image intensification is the leading category, with a 2024 share of 40%, because defense forces require superior low-light tactical visibility for their operations. Users can view in unlit conditions with devices that expand the existing environmental lighting to make objects more visible. The widespread use of the I² technology is visible in night vision goggles, monoculars, and sniper rifle scopes, which military forces heavily rely on.

The technologies analyzed here are:

Image Intensification (I²) (Largest Category)

Thermal Imaging

Infrared (IR) Illumination

Digital Imaging (Fastest-Growing Category)

Others

Mounting Type Analysis

Portable is the leading category with a share of 65% because of their mobility, flexibility, and diverse applications from defense to civilian. Portable devices, such as monoculars, thermal scopes, and night vision goggles, can be easily deployed in fast-paced and dynamic environments, which is why they are preferred by outdoor enthusiasts, law enforcement, and military personnel portable systems. They are majorly used where quick deployment and mobility are critical, such as surveillance, tactical operations, and border security. With the increase in people engaging in recreational activities, including wildlife observation and hunting, the use of portable night vision devices is rising as they are easy to use in remote and rugged areas. Moreover, portable scopes can easily be mounted on sniper rifles in times of a SWAT operation or border skirmish.

The mounting types analyzed here are:

Stationary

Portable (Larger and Faster-Growing Category)

End User Analysis

Government and military agencies dominate the market with 55% revenue as they need advanced and high-performance equipment for tactical operations, reconnaissance tasks, border security, and national defense tasks. The Department of Defense serves as the primary government buyer of night vision goggles, thermal scopes, and infrared imaging devices, particularly for reconnaissance and combat tasks.

Drive strategic growth with comprehensive market analysis

U.S. Night Vision Equipment Market Geographical Analysis

The South region dominates the market with a share of 45% due to its vast military presence, large police forces, and expanding interest in wilderness and recreational pursuits. The Texas and Florida defense and law enforcement sectors have high night vision system requirements primarily for tactical and surveillance purposes. The extensive hunting and ranching communities in this region drive the sale of night vision products for outdoor and recreational activities increases. Moreover, the U.S.–Mexico border is highly volatile, with tens of thousands of illegal immigrants apprehended in night border patrols every month.

The Region Analyzed here are:

Northeast

Midwest

West

South (Largest and Faster-Growing Region)

U.S. Night Vision Equipment Market Competitive Landscape

The market is fragmented as a wide range of players exist, from different sectors from military contractors to recreational product manufacturers. The market in the military segment is controlled mainly by Teledyne FLIR, ATN Corp., and L3Harris Technologies due to their advanced technology. But, many smaller businesses serve hunting, law enforcement, and internal security needs.

Smaller market participants concentrate on making specialized products, including monoculars thermal scopes, and digital night vision systems, more affordable and intuitive. The competition is intense because newer companies are entering the thermal imaging and digital night vision segments of the sector.

Leave a comment